While there are those who understand the real-estate market well, others see it as a…

How to get a good credit score 101

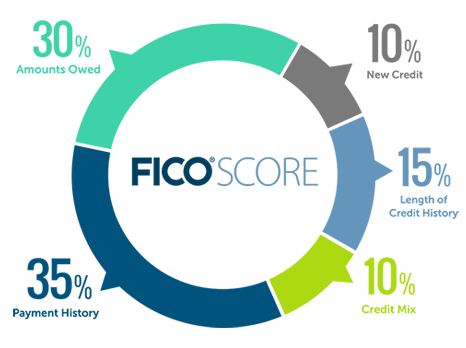

Whether it’s purchasing a home or car, your credit score will be checked. When it comes to purchasing a home, you will need a credit score of at least 580 to qualify for a mortgage. So how exactly can a person increase their credit score? It may be a little more complex than just paying the bills. let’s see the different factors to consider when trying to increase a credit score.

Obtain a free credit report

The best place to start is by finding out what your credit score is. Websites such as annual credit report, and credit karma all offer a free credit score review through their websites. The information that you will need to provide to them are your full name, address, birth date, and social security number. After reviewing your credit report, you will know where you stand and where you need improvements. It is important to review your credit report thoroughly because credit bureaus may make mistakes when compiling a report. For example, you may notice an open account that has been closed already, or someone else’s information on your report. Many people have the same or similar name and the credit bureaus aren’t perfect. Therefore, when applying for a mortgage it’s important to get these mistakes corrected through a rapid re-score.

Avoid late payments

One of the biggest factors to consider when increasing a credit score is making sure that bills are paid on time. Although a mortgage lender may overlook a one (1) 30-day late, late payments will negatively impact a credit score and raise inquiries to lenders. Credit scores are based on a trend ranking, meaning that credit bureaus look at a person’s history of payments and issue a score based on a person’s payment patterns and how many accounts they have open. Should you have a poor payment history riddled with late payments, don’t fret, start making a change today. By making payments on time, you will see your score improve over the course of months. To start making payments on time, keep a calendar, either on paper or on your cell phone. Also, you may want to put some bills on auto-pay, just be careful of auto-pay pitfalls.

Auto-pay

Although auto-pay sounds great to make payments on time, they can become counteractive if you place them on credit cards. The reason for this is because a credit score also takes high balances into consideration. Therefore, if you decide to set up auto pay, it may be a good idea to use a debit card, since it won’t increase your credit cards balance.

Pay down high-balance credit cards

As we went over before, high balance credit cards will negatively impact a person’s credit. With that said, it is a good idea to focus on paying down credit card balances before other debt. Interest rates are the highest among credit cards, and to compound that is the fact that it is revolving, meaning it doesn’t have an end date like a mortgage. It is good practice to pay down the smallest balance credit cards before tackling larger balanced ones. This is because you will be able to pay those smaller cards quicker without becoming overwhelmed with large payments. Also, it allows you to have more money to apply to another card once that first one is payed down.

Don’t open new accounts

Finally, stay away from opening new accounts, since lenders see this as a bad sign. When you open a new account, a lender sees it as you’re taking on more debt and may have a problem paying it off. also, never open a new account when applying for a mortgage because it may lower your DTI (Debt-to-Income ratio), and they may question whether you can afford to pay your new mortgage after buying that new Porsche!

Related Posts